Running payroll in Pakistan requires navigation of federal and provincial tax laws. Ignoring these regulations results in administrative complications that impact your standing with tax entities and change the financial state of your employees.

Each month, you must calculate gross-to-net income, process statutory withholdings, generate pay records, and meet payment deadlines. If a single deduction is missed, your business faces financial penalties, audits, and employee dissatisfaction.

Whether you are establishing a local entity or expanding into Pakistan, this guide outlines required tax obligations. By understanding the link between federal income tax, EOBI pension schemes, and provincial social security institutions, you can structure competitive salary packages that attract personnel while limiting tax liabilities.

What Are Payroll Taxes in Pakistan?

Payroll taxes in Pakistan are mandatory wage deductions and statutory contributions that employers must calculate and transfer to the Federal Board of Revenue (FBR) and regional labor departments. These financial obligations support national welfare programs, including retirement pensions through the Employees’ Old-Age Benefits Institution (EOBI), alongside provincial healthcare and workplace injury coverage.

Employers act as withholding agents, subtracting income tax from employee salaries based on federal tax rates. This operational task is necessary for business success, as accurate, timely filing avoids financial penalties, audit complications, and legal liability, while ensuring that staff receive social benefits. The exact amount of these deductions varies based on annual policy shifts, influencing the final take-home pay for workers across different income levels.

Types of Payroll Taxes in Pakistan

Payroll taxes in Pakistan are mandatory deductions and contributions that employers must manage to comply with the law and provide benefits to employees. These taxes fund important programs like retirement pensions, healthcare, and social security. Knowing the different types of payroll taxes helps businesses stay compliant, avoid fines, and ensure employees get the benefits they deserve.

- Income Tax Withholding: Employers deduct income tax from employees’ salaries every month based on Pakistan’s tax slabs. This deduction is mandatory and depends on the employee’s total taxable income. Employers must calculate the correct tax, withhold it, and submit payments to the Federal Board of Revenue (FBR) on time. Failing to do so can lead to penalties and interest charges. Providing employees with accurate salary certificates helps them file their tax returns smoothly. Proper income tax withholding also prevents surprises during annual tax assessments.

- Employees’ Old-Age Benefits Institution: Employers and employees both contribute to EOBI, which provides retirement pensions, disability benefits, and survivors’ support. Employers pay 5% of the statutory minimum wage, while employees contribute 1% deducted from their wages. Timely monthly payments to EOBI protect workers’ financial security and keep the business compliant. For employees these transfers mean protected income after retirement or in the event of disability, an aspect of the local social safety net.

- Social Security Contributions: Employers contribute to provincial social security funds that cover medical care, maternity benefits, sickness allowances, and compensation for workplace injuries. These contributions protect employees and reduce employer liability in case of accidents or illness. Social security also offers rehabilitation services, helping injured workers return to work faster. Understanding provincial differences in contribution rates and benefits ensures accurate payroll processing and compliance.

- Other Mandatory Deductions: Depending on the province or sector, employers may also deduct professional tax or contribute to local welfare funds like the Workers’ Welfare Fund (WWF). These funds support worker welfare initiatives, including improving workplace safety, providing financial aid during emergencies, and funding skill development programs. Employers should stay updated on local regulations to ensure all required deductions are applied correctly.

Payroll Tax: Employer’s & Employee’s Obligations

Understanding payroll taxes from both the employer’s and employee’s perspectives is essential for accurate payroll tax calculation, smooth compliance, and maintaining workplace trust in Pakistan.

Employer’s Obligations

Employers in Pakistan are required to make several mandatory contributions to social security funds and comply with payroll tax laws. Failure to meet these obligations often leads to common payroll errors, which can result in costly penalties, employee dissatisfaction, and compliance risks. These obligations vary based on fund type and province, making it essential for employers to maintain accurate payroll processes to avoid such errors.

- Employees’ Old-Age Benefits Institution (EOBI): Employers contribute 5% of the declared minimum wage per employee to this federal pension scheme. Employees contribute 1% via salary deductions. Contributions are calculated on the minimum wage floor, regardless of actual salary.

- Provincial Social Security Institutions (PESSI, SESSI, etc.): Employers must contribute a percentage of wages to provincial social security funds providing healthcare and related benefits. Rates vary, typically around 5-7% from employers and 1% deducted from employees, applicable for workers earning below defined wage limits.

- Workers’ Welfare Fund (WWF): Employers with annual income above a specific threshold contribute 2% of total income. This fund supports worker welfare programs and is primarily for industrial enterprises.

- Workers’ Participation Fund (WPF): Companies meeting capital or asset thresholds contribute 5% of net profits, distributed as profit-sharing to eligible employees.

- Compliance Requirements: Employers must register employees with EOBI and provincial bodies, calculate contributions accurately, submit payments timely, and maintain proper records to avoid penalties.

- Financial Impact: Employer contributions add approximately 6-7% on top of gross salaries, affecting overall employment costs and requiring budget planning.

Employee’s Obligations

Employees in Pakistan are subject to several payroll deductions and responsibilities that directly impact their take-home pay and social benefits.

- Income Tax Withholding: Monthly income tax is deducted at source according to the current tax slabs. Employees earning up to PKR 600,000 per year are exempt, while higher earners contribute more. This ensures steady compliance with FBR requirements and reduces end-of-year tax liabilities.

- Social Security Deductions: A small portion of wages is deducted for provincial social security funds, granting employees access to essential benefits like medical care, hospitalization, maternity leave, and disability coverage. These schemes support employees during illness or workplace injury.

- EOBI Contributions and Pension Security: Employees contribute 1% of the declared minimum wage per month to the Employees’ Old-Age Benefits Institution (EOBI), while employers contribute a higher percentage. These deductions help build eligibility for retirement pensions, survivor benefits, and disability support.

- Zakat Deductions: For Muslim employees, zakat is automatically deducted by employers if the employee’s assets reach the nisab threshold on the 1st of Ramadan. This deduction is recognized under Pakistan’s tax laws and reduces the employee’s taxable income, helping fulfill religious and legal obligations.

- Payslip Transparency: Employees have the right to receive clear payslips listing gross salary, all deductions (including tax, zakat, and social security), and net pay. This enables them to verify their earnings and address any issues promptly.

- Claiming Deductions and Tax Credits: Employees can maximize their net income by submitting documentation for eligible tax deductions or credits (such as investments in pension funds, charitable donations, zakat, and qualifying educational expenses) to their employer for accurate monthly withholding.

Payroll Tax for Foreign Companies in Pakistan

Foreign companies operating in Pakistan handle complex payroll requirements that vary from those of local entities. Maintaining full legal standing requires a solid grasp of tax residency, international agreements, and local labor rules.

- Permanent Establishment (PE) Status: Foreign entities must determine if their operations represent a PE in Pakistan. A PE triggers registration with the Federal Board of Revenue (FBR) and full payroll tax compliance obligations.

- FBR Registration & Tax Withholding: Once registered, foreign companies must withhold income tax from employee salaries as per Pakistan’s progressive tax slabs and remit those taxes timely to the FBR.

- Provincial Social Security Contributions: Depending on local hire or secondment status, foreign companies may need to contribute to provincial schemes like PESSI or SESSI, which provide healthcare and welfare benefits.

- Expatriate Employee Taxation: Payroll taxation for expatriates depends on tax residency and duration of stay; specialized planning is needed to ensure compliance and optimize liability.

- Use of Local Payroll Providers: Given the complexity, many foreign companies outsource payroll operations to local experts to assure accurate tax calculation, filing, and compliance.

- Currency & Payment Compliance: Employers should pay salaries in Pakistani Rupees through regulated local banking channels to comply with currency and anti-money laundering laws.

- Double Taxation Conventions (DTCs): Pakistan has Double Taxation Agreements (DTAs) with over 66 countries to prevent the same income being taxed twice. DTCs allocate taxing rights between source and residence countries to avoid double taxation and offer relief through exemptions or tax credits. These treaties reduce withholding tax rates on dividends, interest, and royalties, often capped at 5-10%, aiding foreign businesses in managing their tax burden.

Regular Reporting & Compliance: Foreign companies must file monthly payroll tax returns through the FBR’s IRIS portal, ensuring accurate and timely submission to avoid penalties.

Payroll Tax Rates and Updates for 2026 in Pakistan

The Government of Pakistan has introduced new payroll tax rates and income tax slabs for salaried individuals through the Finance Act 2026, effective from July 1, 2026, to June 30, 2027. These changes aim to provide relief to low and middle-income earners by lowering tax rates while maintaining a progressive structure that ensures higher earners contribute a fair share.

Latest Income Tax Slabs for Salaried Individuals (FY 2025-26)

| Annual Taxable Salary (PKR) | Annual Tax Rate / Formula |

| Up to 600,000 | 0% |

| 600,001 – 1,200,000 | 1% of the amount exceeding 600,000 |

| 1,200,001 – 2,200,000 | 6,000 + 11% of the amount exceeding 1,200,000 |

| 2,200,001 – 3,200,000 | 116,000 + 20% of the amount exceeding 2,200,000 |

| 3,200,001 – 4,100,000 | 316,000 + 25% of the amount exceeding 3,200,000 |

| 4,100,001 – 5,600,000 | 541,000 + 29% of the amount exceeding 4,100,000 |

| 5,600,001 – 7,000,000 | 976,000 + 32% of the amount exceeding 5,600,000 |

| Above 7,000,000 | 1,424,000 + 35% of the amount exceeding 7,000,000 |

These updates provide tax relief across various income levels. The revised slabs offer lower liability for middle-income earners through updated percentage formulas, while the removal of the 9% surcharge for top-tier earners increases net take-home pay.

By modifying the tax brackets and adjusting rates for mid-to-high earners, the government aims to support household purchasing power while maintaining the funds required for public services.

Key Payroll Tax Updates and Compliance Requirements

With the Finance Act 2026, changes to payroll taxation for the 2026-27 fiscal year are in effect. Employers and employees must adopt these updates to ensure legal compliance and accurate payroll processing.

- Revised Income Tax Slabs: The government introduced eight tax brackets to offer tax reductions to middle and upper-middle income earners. While the tax-free threshold stays at PKR 600,000, new percentage categories were implemented to manage income levels.

- Removal of the Surcharge: The 9% surcharge previously applied to annual taxable incomes exceeding PKR 10 million is no longer in effect. High-income professionals and senior executives may not face this additional levy, simplifying tax calculations for payroll.

- Maximum Tax: The top tax rate of 35% is adjusted. Under the 2026-27 rules, this rate applies only to annual taxable income exceeding PKR 7 million. This provides a larger gap compared to the previous threshold of PKR 4.1 million.

- Payroll System Updates: Employers must update their payroll systems to use these new tax tables. Accurate withholding and timely submission to the Federal Board of Revenue (FBR) are required to prevent interest charges and administrative penalties.

- Payslip Transparency: Companies must issue payslips that detail all deductions. This practice allows staff to verify their net earnings and confirms that the correct tax amounts are withheld under the 2026-27 framework.

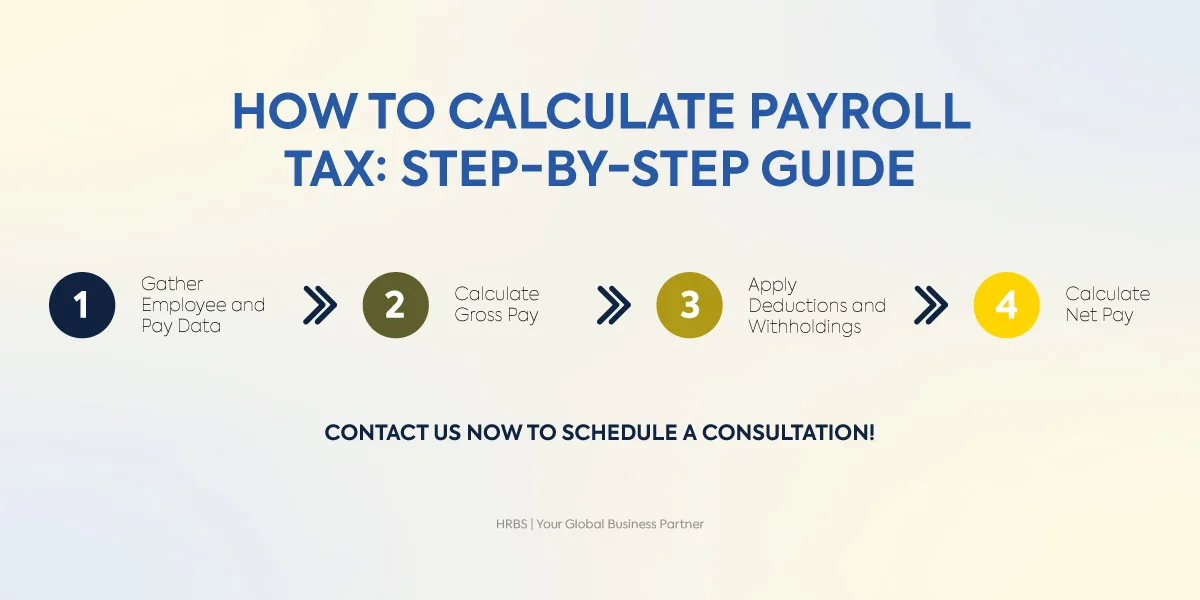

How to Calculate Payroll Taxes in Pakistan

Accurate payroll tax calculation is crucial for compliance and ensuring employees receive the correct pay. Here’s an updated step-by-step process for calculating payroll tax in Pakistan for the fiscal year 2025-26:

Step 1: Gather Employee and Salary Details

Collect all necessary employee information including:

- Basic salary

- Allowances (housing, medical, conveyance)

- Bonuses and overtime payments

- Any other taxable benefits or deductions (e.g., provident fund, loan repayments)

- Accurate data collection is crucial for precise payroll calculations and tax compliance.

Step 2: Calculate Gross Salary

Add the basic salary, allowances, bonuses, and overtime to determine the employee’s gross salary. For salaried employees, this typically includes fixed monthly pay plus any additional earnings.

Step 3: Calculate Income Tax Deduction

Using the 2025-26 progressive tax slabs effective July 1, 2025, calculate income tax:

- Up to PKR 600,000 annual income: 0% tax

- PKR 600,001 – 1,200,000: 1% of the amount exceeding 600,000

- PKR 1,200,001 – 2,200,000: PKR 6,000 + 11% of the amount exceeding 1,200,000

- PKR 2,200,001 – 3,200,000: PKR 116,000 + 20% of the amount exceeding 2,200,000

- PKR 3,200,001 – 4,100,000: PKR 316,000 + 25% of the amount exceeding 3,200,000

- PKR 4,100,001 – 5,600,000: PKR 541,000 + 29% of the amount exceeding 4,100,000

- 5,600,001 – 7,000,000: PKR 976,000 + 32% of the amount exceeding 5,600,000

- Above 7,000,000: PKR 1,424,000 + 35% of the amount exceeding 7,000,000

Calculate the monthly equivalent by dividing the annual tax by 12 for monthly withholding.

Step 4: Deduct Other Statutory Contributions

Subtract mandatory deductions such as:

- 1% Employees’ Old-Age Benefits Institution (EOBI) contribution from the employee’s salary

- Provident fund contributions (if applicable)

- Any other statutory or company-specific deductions

Step 5: Calculate Net Salary

Subtract total deductions (income tax + statutory contributions + other deductions) from the gross salary to determine the net salary payable to the employee.

Example

An employee earns:

- Basic salary: PKR 100,000

- Housing allowance: PKR 20,000

- Medical allowance: PKR 5,000

- Gross Salary: PKR 125,000

- Monthly equivalent exemption = PKR 50,000 (PKR 600,000 annual exemption / 12)

- Taxable amount = PKR 125,000 – PKR 50,000 = PKR 75,000

- Income tax = 1% of 75,000 = PKR 750

- EOBI contribution (1%) = PKR 1,250

- Total deductions = PKR 2,000

Net salary = PKR 125,000 – PKR 2,000 = PKR 123,000

Also Read: How to calculate payroll costs.

Payroll Tax Filing Deadlines and Documentation Requirements

Timely payroll tax filing and maintaining accurate documentation are crucial for compliance with Pakistan’s tax laws and avoiding penalties. Employers must understand the key filing deadlines and keep all necessary paperwork organized.

- Monthly Tax Filing Deadline: Employers are required to deduct and deposit payroll taxes, including income tax withholding, EOBI, and provincial social security contributions, by the 15th day of the month following the salary payment. For instance, tax deductions on salaries paid in June must be filed and paid by July 15.

- Annual Salary Certificates (Form 16): Employers must issue detailed salary certificates to employees by August 31 each year. These certificates summarize total earnings, tax deductions, and other payroll information, enabling employees to accurately file their annual income tax returns.

- Required Documentation: Employers should maintain comprehensive records such as employee copies of CNIC, monthly payroll registers with salary, allowances, and tax deductions, tax deduction certificates provided to employees, and proof of tax deposits and challans submitted to both the Federal Board of Revenue (FBR) and provincial social security institutions. These records should be preserved for at least five years to satisfy audit and compliance reviews.

- Electronic Filing via IRIS Portal: The FBR encourages electronic filing of payroll taxes and income tax returns through its IRIS portal. E-filing enhances accuracy, accelerates processing, and offers instant confirmation of submission, reducing the chances of errors and late penalties.

How Payroll Taxes Affect Freelancers and Contract Workers

Freelancers and independent contractors in Pakistan have distinct payroll tax responsibilities compared to salaried employees, including self-assessment tax filing, managing withholding tax on payments, and registering with tax authorities like the FBR and Pakistan Software Export Board (PSEB). Understanding these differences is essential not only for legal compliance and tax optimization but also for maximizing access to government incentives and ensuring sustainable financial planning in Pakistan’s rapidly growing freelance economy.

- Self-Assessment and Tax Filing: Freelancers are responsible for calculating and paying their own income tax based on their business income. They must file annual income tax returns with the Federal Board of Revenue (FBR), declaring all earnings from freelancing activities, including payments received from both domestic and international clients.

- Withholding Tax on Payments: Payments to freelancers may be subject to withholding tax. Registered freelancers with the PSEB benefit from reduced withholding tax rates (as low as 0.25%), while non-registered freelancers face higher flat rates (up to 1%).

- Tax Registration: Freelancers must register with the FBR to obtain NTN, which is mandatory for filing taxes and accessing various benefits. Additionally, IT and digital service freelancers earning from international clients are encouraged to register with the PSEB. It offers a significant tax benefits, including eligibility for tax credits, reduced withholding tax rates, and access to government grants and support programs.

- Record-Keeping Requirements: Maintaining detailed invoices, bank statements, receipts, and expense records is critical. Proper documentation allows freelancers to claim allowable business expenses, reducing taxable income and optimizing tax liabilities.

- No Employer Social Security Contributions: Unlike salaried employees, freelancers do not receive employer-funded social security benefits like pensions or medical coverage. They must independently secure private insurance and retirement savings plans.

Common Payroll Tax Mistakes and How to Avoid Them

Payroll tax mistakes in Pakistan can cause costly financial penalties and legal issues. These errors often arise due to outdated payroll systems, lack of staff training, or misunderstanding tax laws. Key mistakes to avoid include:

- Incorrect Application of Tax Slabs: Incorrect tax slab application happens when employers fail to update payroll systems with the latest progressive tax rates or misclassify employee income. This leads to wrong tax withholding—either overcharging or undercharging employees. Ensure payroll software is regularly updated and all salary components, including allowances and bonuses, are correctly included.

- Misclassification of Taxable Allowances: Misclassifying taxable allowances like conveyance and medical allowances inflates tax liabilities unnecessarily. Employers should distinguish between taxable and exempt benefits according to current Pakistan tax rules to avoid excess deductions.

- Ignoring Provincial Social Security Contributions: Ignoring provincial social security contributions is another common error. Contribution rates vary by province—such as 7% for Punjab’s PESSI and 6% for Sindh’s SESSI—so employers must apply correct rates to stay compliant.

- Late Submission of Payroll Taxes: Late payroll tax submissions result in fines and interest from FBR and provincial institutions. Automate your payroll schedule, use electronic filing systems like FBR’s IRIS portal, and set internal reminders to meet deadlines.

- Inadequate Payroll Record-Keeping: Poor payroll record-keeping with incomplete payslips, missing tax certificates, or absent employee CNIC copies complicates audits and legal compliance. Keep detailed, accurate records for at least five years as required by law.

How HRBS Can Help With Payroll Services Across Pakistan?

Managing payroll taxes in Pakistan involves complex federal and provincial regulations. Non-compliance often leads to costly penalties and legal risks. HRBS provides expert, local payroll solutions that keep your business compliant while ensuring your workforce is paid accurately and on time.

- Accurate Payroll Calculations: We use advanced software and knowledge of Pakistan’s current tax slabs and labor laws. Our team ensure every salary component, allowance, and statutory deduction is calculated correctly according to the latest regulations.

- Tax Filings and Payments: Our team manages all payroll tax obligations, including income tax withholdings, EOBI contributions, and provincial social security. We meet all monthly and annual deadlines to protect your business from fines and audit complications.

- Transparent Payslips: We provide detailed payslips that clearly show all earnings and deductions. This transparency helps your employees verify their net pay and understand how their salary is calculated under current tax rules.

- Data Security: Our team protects sensitive information with strict security protocols. We follow industry data protection standards to keep employee payroll records safe at all times.

- Dedicated Expert Support: Our payroll specialists provide responsive guidance to answer your questions and update your payroll processes as laws change.

Take the stress out of payroll management partner with HRBS today for expert, compliant, and accurate payroll solutions tailored to Pakistan’s unique regulations.

FAQs

What are the current income tax slabs for salaried individuals in Pakistan for FY 2026-27?

For the fiscal year 2026-27, Pakistan employs a progressive tax system for salaried individuals under the Finance Act 2026, effective since July 1, 2026. Annual income up to PKR 600,000 remains tax-exempt. For earnings above this threshold, tax rates apply in tiers: 1% for income between PKR 600,001 and PKR 1,200,000, followed by incremental rates of 11%, 20%, 25%, 29%, 32%, and reaching a maximum of 35% for annual incomes exceeding PKR 7,000,000. These updated brackets simplify payroll calculations by removing the previous 9% surcharge for high earners and adding new percentage steps to ensure a gradual increase in tax liability. This system aims to support household purchasing power while collecting the funds required for public services.

What are the key payroll tax filing deadlines employers must follow in Pakistan?

Employers are required to deduct payroll taxes, including income tax and social security contributions, and deposit these amounts with FBR by the 15th day of the month following salary payments. Furthermore, employers must issue annual salary certificates, known as Form 16, to their employees no later than August 31 each year. These certificates assist employees in accurately completing their income tax returns.

Are bonuses and incentives subject to payroll tax in Pakistan?

Yes, bonuses and incentives such as performance bonuses, cash incentives, commissions, and other taxable allowances are considered part of an employee’s taxable income and are subject to payroll tax deductions. Employers must include all such monetary benefits alongside the regular salary when calculating monthly withholding tax based on the applicable progressive tax slabs.

Are freelancers and contract workers subject to payroll tax deductions in Pakistan?

Freelancers and contract workers in Pakistan are obligated to self-assess and pay their income tax. While clients may deduct withholding tax on payments made to freelancers, these workers must register with the FBR themselves, file annual income tax returns, and maintain detailed records of income and allowable expenses. Although freelancers do not fall under traditional payroll tax withholding by employers, ensuring proper registration and tax filing is critical for compliance with Pakistan’s tax laws.

What supporting documents must employees submit to claim payroll tax deductions or credits?

To claim payroll tax deductions or credits, employees need to submit valid documentation such as receipts for approved pension fund contributions, certified proofs of charitable donations including zakat, records for educational expenses where deductions apply, and medical certificates relating to allowable health expenses. Submitting these documents ahead of payroll processing deadlines enables employers to adjust tax withholding amounts accordingly, maximizing employee take-home pay while maintaining compliance with FBR policies.

What social security benefits do payroll tax deductions fund for employees in Pakistan?

Payroll tax deductions in Pakistan fund essential social security benefits, including medical care, hospitalization, specialist consultations, maternity leave, and compensation for workplace injuries through provincial institutions like PESSI and SESSI. Additionally, retirement pensions and disability benefits are provided via the EOBI.

Can employers outsource payroll tax management in Pakistan, and what are the advantages?

Many employers in Pakistan choose to outsource payroll tax management to specialized professional service providers. This approach ensures accurate tax calculations, timely compliance with ever-changing tax laws, and the efficient filing of monthly and annual returns. Outsourcing reduces the administrative burden on companies, minimizes audit and penalty risks, and provides access to expert guidance on complex payroll matters, improving overall payroll accuracy and regulatory adherence.

How are payroll taxes handled for expatriate employees working in Pakistan?

The taxation of expatriate employees working in Pakistan depends on their resident or non-resident status and length of stay. Residents are taxed on their global income, whereas non-residents are taxed only on Pakistan-sourced earnings. Employers must apply the correct withholding tax in line with local tax slabs, taking into account any exemptions or benefits available under Double Taxation Agreements (DTAs). Special attention is also given to the treatment of allowances, reimbursements, and social security contributions under local labor contracts.

What are the penalties for late or non-filing of payroll and income tax returns in Pakistan?

Failure to file payroll taxes or income tax returns on time results in significant penalties imposed by the Federal Board of Revenue. These penalties include daily fines, fixed monetary fines, and interest on overdue tax payments. Non-filers may also be subjected to higher withholding tax rates on various financial transactions such as property purchases and banking activities. Timely and accurate filing is crucial to avoid financial loss and adverse legal consequences.